I was recently asked by a provider, who was involved in an audit, whether she may have been flagged because her fees were “too high.”

When I asked how she set her fees, she said:

“My biller gave them to me.” Oh my.

Your fee schedule is your business decision. It should not be randomly created by someone else, especially if your biller is percentage-based and earns more when charges are higher.

And yet, I see this happen all the time.

A fee schedule is not just a list of prices. It affects patient communication, insurance reimbursement, out-of-network collections, audits, compliance risk, and the financial health of your practice.

What Should You Consider When Setting Fees?

There are different ways to create a fee schedule, but before you pick numbers, you should think through several important factors:

- Your actual cost per visit

- This includes rent, supplies, staff, software, merchant fees, billing costs, taxes, malpractice insurance, laundry, equipment, and your own time.

- Local market rates

- It is helpful to know what other clinics in your area charge, but do not blindly copy them. Their overhead, visit length, contracts, and business model may be completely different from yours.

- Whether your fees are defensible

- If your fees are extremely high, carriers may question whether you are actually collecting the full patient responsibility. This is especially true for out-of-network providers.

- A fee for each service you provide

- You should have a fee for each service, including acupuncture, exams, manual therapy, therapeutic exercise, cupping, herbs, supplies, forms, missed appointments, and any other services you provide.

- Separate insurance and cash/time-of-service rates

- Your insurance fee schedule and your cash fee schedule should be clearly defined and consistently applied.

Time-of-Service Cash Fees

Your time-of-service cash fees are often lower than your insurance fees because you are not billing a claim, waiting for reimbursement, following up on denials, or managing insurance delays.

A common approach is to set your time-of-service cash rate at approximately 20% less than your insurance fee schedule.

This type of discount is based on the reduced administrative cost of not billing insurance. It should be written into your office policy and applied consistently.

One Way to Create Your Fee Schedule

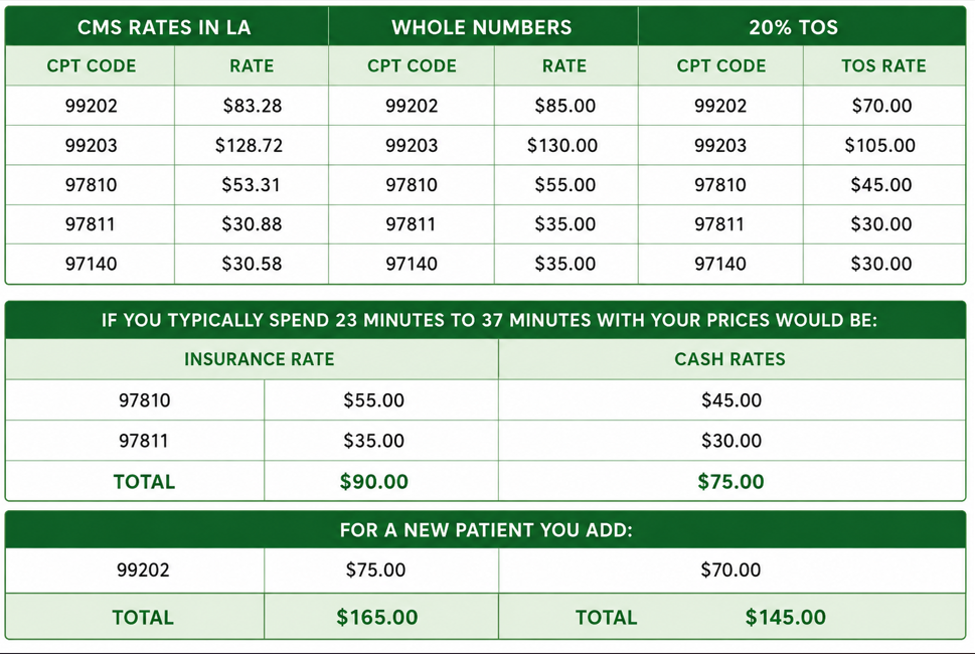

One method is to use Medicare rates as a starting point.

You can look up fees for your geographic area using the CMS Physician Fee Schedule Search Tool: https://www.cms.gov/medicare/physician-fee-schedule/search

For this example, I used the Los Angeles area and estimated a face-to-face visit of approximately 30 minutes.

The first column shows the CMS allowable amounts. CMS works with the AMA and other data sources to value CPT codes and estimate the relative cost of providing services. Some providers may find Medicare rates too low, and that is fine. This is simply a starting point for the exercise.

From there, I rounded the fees to cleaner whole numbers, always slightly above the Medicare allowance. Then I calculated the time-of-service cash rate by reducing the whole-number fee by approximately 20%.

Check the Local Market

After creating the sample fee schedule, I checked local clinics in the area that publicly posted their prices.

Their cash prices were generally listed as:

First visit: $150–$180

Follow-up visit: $80–$100

That told me the sample rates were in the ballpark.

You could then repeat this same exercise using 120% of Medicare, 130% of Medicare, or another reasonable benchmark until you create a complete fee schedule that makes sense for your practice.

The goal is to create:

- An insurance fee schedule

- A time-of-service cash fee schedule

- A clear written policy explaining how each is used

Why the 20% Difference Matters

You want your cash discount to be reasonable and explainable.

You also want your insurance fees to be high enough that, for out-of-network carriers, you can collect the true patient coinsurance amount.

Here is where some providers get into trouble.

I have seen providers bill a new patient visit at something like $350 for a scenario that may be more reasonably valued around $165.

I call this the “slap it against the wall and see what sticks” approach.

Let’s say the carrier pays $200 on that $350 claim. That leaves a $150 patient responsibility. The office is then expected to collect that $150 from the patient.

But many offices that bill this way do not actually collect the full coinsurance.

That creates a problem.

Carriers may ask for proof that the patient responsibility was collected. If the office cannot show that it collected the coinsurance, the carrier may argue that the billed fee was inflated or that the provider was not truly charging the patient that amount.

That is when the office can find itself in trouble.

The Bottom Line

Your fee schedule should not be random. It should not be handed to you by your biller without discussion. And it should not be based on “what you hope the carrier will pay.”

A good fee schedule should be:

Consistent

Defensible

Based on your costs

Reasonable for your market

High enough to avoid underbilling

Not so inflated that it creates collection or audit risk

Supported by a clear written financial policy

Your fee schedule is not just about what you charge.

It is part of how you run your practice.